By Bosphorus News Energy Desk

Türkiye's next wind phase will be measured by more than turbine capacity. Batteries, cables, converters, substations, grid software and finance will decide how much of the country's new renewable power becomes usable electricity.

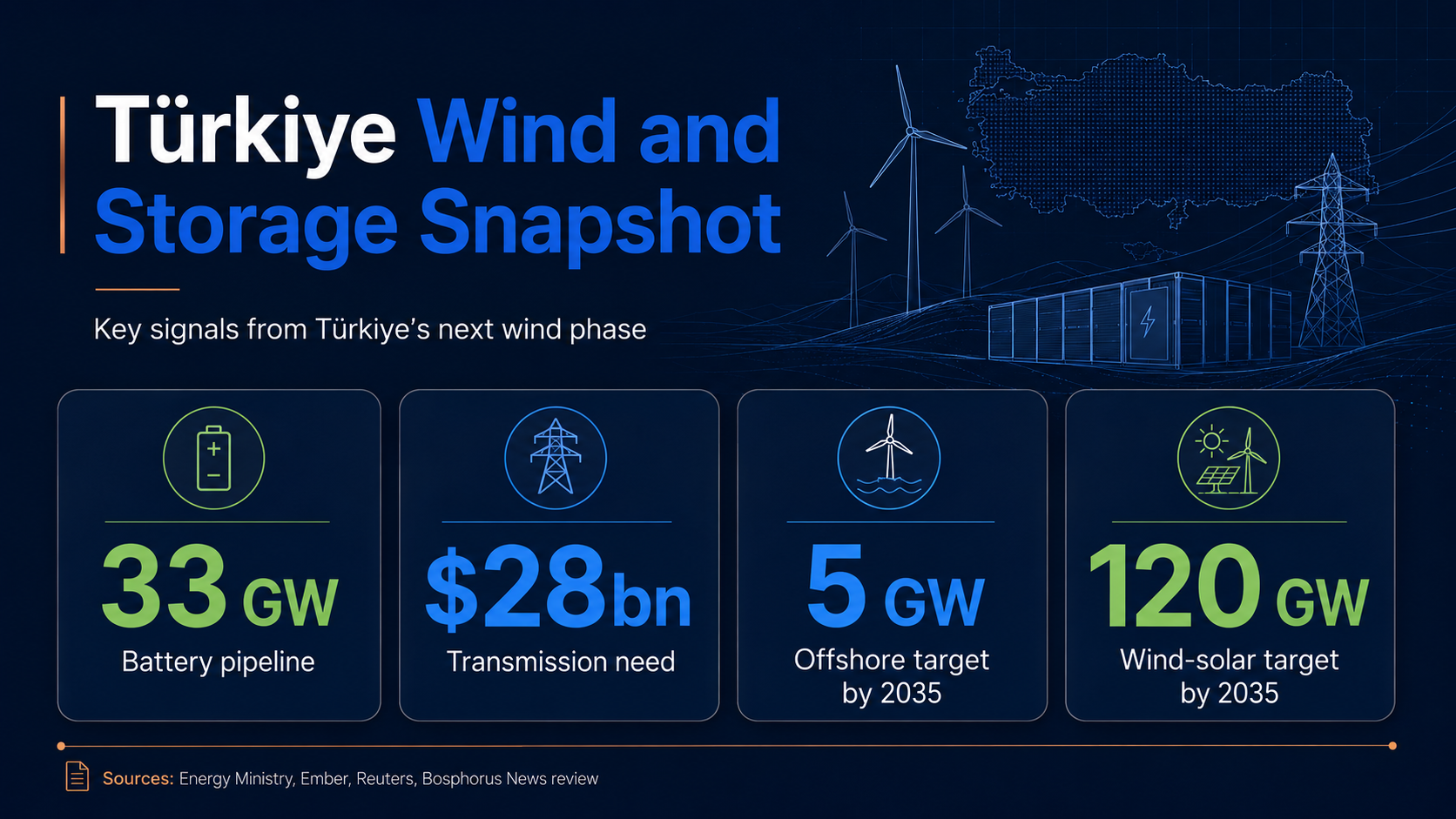

The country is preparing 1,500 MW of wind capacity for 2026 Renewable Energy Resource Area (YEKA) tenders, has identified offshore wind areas near Saros Gulf, Gökçeada, Bozcaada and Edremit, and is targeting 5 GW of offshore wind capacity by 2035. Those targets are the visible edge of a larger shift. Türkiye's wind transition has moved beyond the wind-farm boundary into battery storage, grid equipment, high-voltage transmission, offshore engineering, software, project finance and domestic energy manufacturing.

The onshore scale is already there

Türkiye is no longer an early-stage wind market; its onshore base is large enough to create demand beyond generation assets.

The country's wind capacity is near the 16 GW threshold, placing it well above the regional comparison markets in this report. Greece had about 5.7 GW of installed wind capacity at the end of 2025, while Israel is not a wind-scale comparison at all. Israel's renewable transition is solar-led; its relevance here is grid congestion, storage demand and system adaptation.

That distinction matters. Türkiye's next wind cycle starts from an existing onshore base. The question is no longer limited to who builds wind farms. It is who connects them, stores the power, manages variable output, finances the infrastructure and captures more of the equipment and services chain.

The 33 GW battery signal

Battery storage is the data point that changes the commercial reading of Türkiye's wind market.

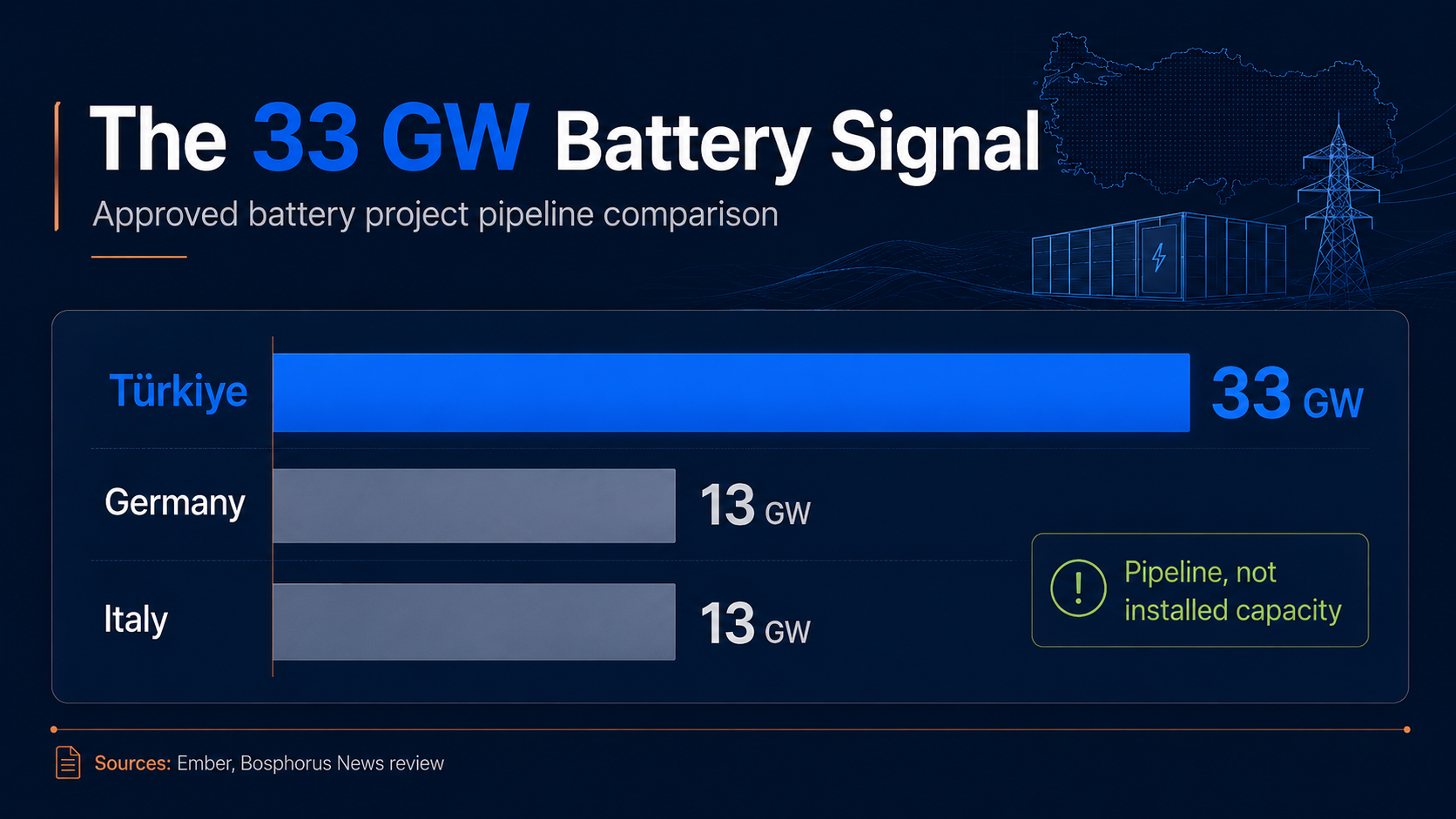

Ember's 2026 Türkiye Electricity Review places Türkiye's approved battery project pipeline at 33 GW, larger than any single European Union market and well above Germany and Italy, each around the 12-13 GW range. The figure is not installed capacity. It is a market-positioning signal for developers, financiers, equipment suppliers, software providers and grid planners.

Bosphorus News reported earlier that Türkiye's approved battery pipeline had already outranked major EU markets before COP31 in Antalya. In this report, that pipeline is treated as a system signal: storage is moving from accessory technology to core infrastructure.

The delivery test remains open. Approved projects must secure financing, grid connection, battery supply, inverter systems, engineering, procurement and construction capacity, commercial operation and dispatch rules. That is why the 33 GW figure matters. It does not close the market story; it opens it.

The grid bill behind wind growth

Türkiye's wind transition is now an infrastructure question as well as a generation question.

The country's 2035 roadmap targets 120 GW of wind and solar capacity. Reuters has reported that the plan requires about $108 billion in investment, including $28 billion for transmission infrastructure. Türkiye has also opened talks with the World Bank for up to $6 billion in electricity-transmission financing, including high-voltage direct current (HVDC) investments.

Generation is only the first line of the bill.

The next phase creates demand for HVDC lines, converter stations, AC network expansion, substations, transformers, cable systems, protection systems, balancing tools, battery integration and grid software. For suppliers and financiers, the wind market is widening into the electricity system itself.

A larger wind and solar base requires companies that can move, convert, store, forecast and balance electricity. The value chain is no longer contained inside the wind farm.

Offshore wind returns, but execution is the market

Türkiye's offshore wind file is opening again, but the bankable market sits in the execution chain: measurement, marine surveys, permitting, environmental review, subsea cables, port logistics, floating foundations, offshore engineering and long-term finance.

The lesson from 2018 matters. Türkiye's first offshore wind tender attempt was cancelled after weak investor interest and problems later identified in sector and development-bank assessments: limited site-specific data, permitting uncertainty, high financing costs and competition from cheaper onshore wind and solar.

The current phase is more concrete. Türkiye has identified offshore wind areas near Saros Gulf, Gökçeada, Bozcaada and Edremit. The World Bank estimates Türkiye's technical offshore wind potential at 75 GW, while the official offshore target stands at 5 GW by 2035.

That does not make offshore wind an easy capacity story. Türkiye has no commercial offshore wind capacity yet. Many of the stronger offshore areas are technically demanding, and floating technology may become part of the medium-term equation. The opportunity begins before turbines are installed: data, permits, cables, ports, vessels, engineering and finance all have to arrive first.

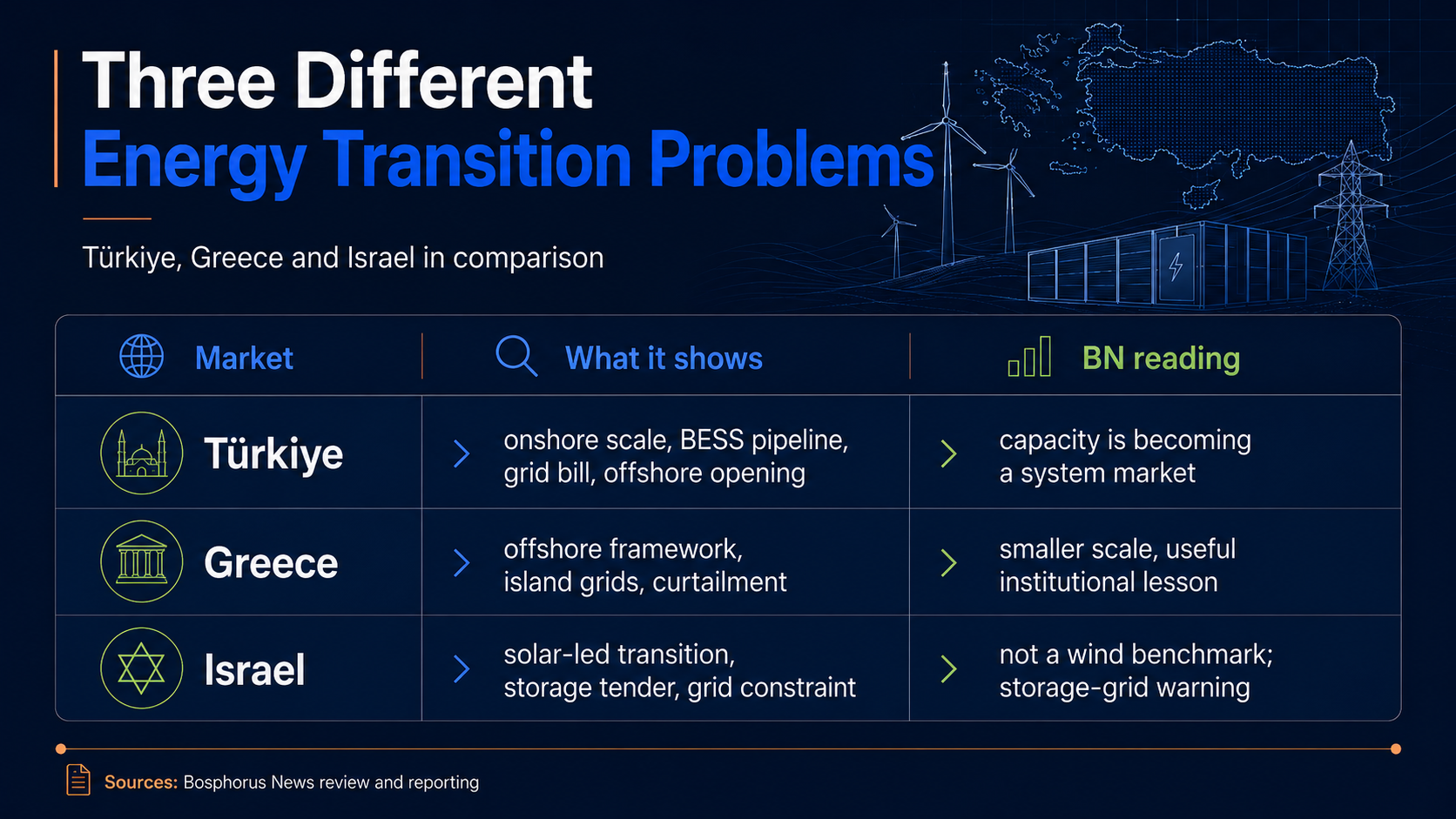

Greece and Israel show different lessons

Greece is not a scale comparison for Türkiye's wind market. It is an institutional and grid comparison.

The Greek wind market is smaller, but Greece has moved earlier on the institutional side of offshore wind, with an official target of around 2 GW of offshore wind capacity by 2030 and an offshore framework led by the Hellenic Hydrocarbons and Energy Resources Management Company. Greece also offers lessons from island interconnections, curtailment pressure and the cost of moving renewable electricity through a fragmented grid geography.

The Crete-Attica high-voltage link, a 1 GW class mainland connection, shows how island-grid constraints can become major infrastructure markets. For Türkiye, the Greek comparison is not about total wind capacity. It is about permitting sequence, marine planning, interconnection and the infrastructure that must arrive before offshore capacity becomes bankable.

Israel offers a different warning.

Israel is not a wind benchmark for Türkiye. It is a storage-grid benchmark. Its renewable system is overwhelmingly solar-led, and wind remains marginal. Israeli reporting says renewable electricity supplied about 16% of the country's power in 2025, missing the 20% target for that year, while the 2030 target remains 30%.

The system constraint is clear: renewable targets can move faster than grids. Israel awarded 1.5 GW of battery storage capacity in 2025, while Israel Electric Corporation secured a $14 billion, 45-year loan for grid expansion. Israel's lesson is that renewable targets become real only when grids, storage and dispatch rules are built fast enough to carry them.

Eight markets inside Türkiye's wind transition

Türkiye's next wind phase speaks to a wider market than wind development.

Battery storage is the first lane. A 33 GW project pipeline creates demand for battery energy storage systems, inverters, power electronics, system integration, engineering and finance.

Transmission and HVDC infrastructure form the second lane. The $28 billion transmission need points to cable systems, converter stations, high-voltage engineering, substations and long-term network planning.

Substations and grid hardware form a third market. Transformers, switchgear, protection systems and connection equipment become more valuable as renewable projects move from capacity allocation into physical grid delivery.

Grid software is the fourth lane. Forecasting, dispatch, balancing, curtailment management and data-driven system operation will become more important as wind and solar output expands.

Offshore engineering is the fifth. Marine surveys, geotechnical work, floating foundations, subsea cables, offshore installation and environmental review will shape whether Türkiye's offshore target becomes a bankable market.

Port and logistics infrastructure form the sixth lane. Offshore wind requires heavy-lift handling, staging areas, cable logistics, vessel access and coastal industrial planning.

Finance and legal structuring are the seventh. Project finance, green bonds, power-purchase agreements, permitting, regulatory advisory and risk allocation will decide which pipelines move into construction.

Domestic manufacturing is the eighth. Wind components, battery packs, power electronics, cable, transformer supply chains and industrial zones all sit inside the next phase if Türkiye captures more of the value chain.

The commercial prize is no longer limited to wind-farm ownership. It sits in the infrastructure and services around wind: batteries, cables, converters, substations, software, offshore engineering and finance.

The market is large, but delivery is the test

The size of the opportunity will be decided by conversion: whether approved pipelines become financed, connected and operating assets.

The 33 GW storage pipeline is a market signal, but it will not become a market outcome without capital, equipment, connection rights, dispatch rules and execution capacity. Offshore wind carries the same challenge. Technical potential and named areas do not automatically create bankable projects.

The grid adds another constraint. Renewable capacity can outpace transmission, and storage duration may not solve every system need. Ember has also warned that a purchase guarantee for domestic coal plants starting in 2026 could increase utilisation rates, complicating the market signal as Türkiye expands renewable capacity and storage-linked project development.

In Türkiye's wind transition, constraints are not only risks. They are also the market: finance, grid connection, engineering, permitting and system integration.

The system will decide the market

Türkiye's wind market is moving from capacity growth into system delivery. The country has an onshore wind base near the 16 GW threshold, named offshore wind areas, a 5 GW offshore target for 2035, a 33 GW battery project pipeline and a transmission roadmap tied to the 120 GW wind-solar target.

Those pieces create a larger market than wind development alone. The next phase will need batteries, cables, converters, substations, software, offshore engineering, project finance and regulatory execution.

Türkiye's next wind phase will not be won by turbine count alone. It will be won by the companies that can connect, store, balance and finance the electricity those turbines produce.

The market beyond turbines is now the real prize.

Sources: Türkiye's Energy and Natural Resources Ministry, World Bank, Ember, Reuters, Global Wind Energy Council, Türkiye Wind Energy Association, HEREMA, IPTO, Times of Israel, Bosphorus News review and reporting.