The latest olive sector statistics and forecasts released by the International Olive Council (IOC) indicate a sharp rebound in global olive oil production following consecutive drought-hit seasons, with Türkiye emerging as one of the most consequential producers in the current cycle.

According to the IOC's December 2025 statistical update, world olive oil output rose strongly in the 2024/25 crop year and is expected to remain historically elevated in 2025/26, easing supply pressures that had driven prices to record levels across major producing regions.

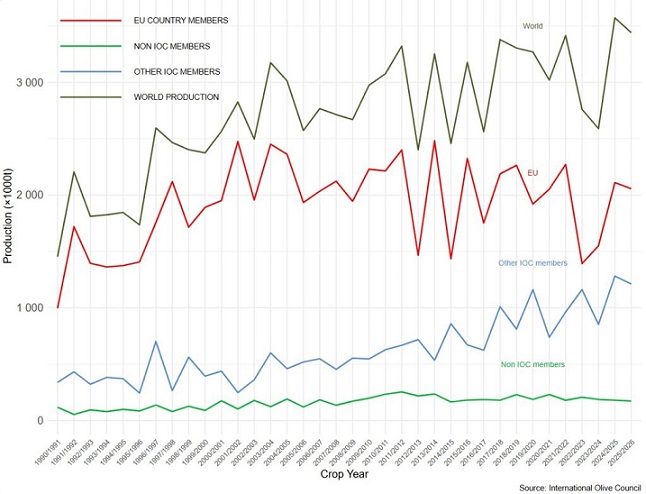

Global production: recovery after scarcity

IOC data show global olive oil production rising from approximately 2.59 million tonnes in 2023/24 to around 3.57 million tonnes in 2024/25, a year-on-year increase of nearly 40 percent. For 2025/26, production is forecast at about 3.44 million tonnes, signalling a modest correction but still well above recent drought-affected averages.

This rebound reflects improved climatic conditions across several Mediterranean producers and a partial recovery in yields following two years of severe water stress.

Consumption and trade stabilise

Global consumption is estimated at roughly 3.2 million tonnes in 2024/25, up around 15 percent from the previous season. The IOC expects international trade volumes to remain robust, with imports and exports each exceeding 1.2 million tonnes in the coming crop year, underscoring olive oil's continued role as a globally traded staple rather than a purely regional product.

Türkiye: from volatility to structural weight

For Türkiye, the data are particularly significant.

The IOC estimates Türkiye's olive oil production at approximately 505,000 tonnes, representing one of the largest year-on-year increases among major producers. This places Türkiye firmly among the top global suppliers and strengthens its position within both Mediterranean and non-EU export markets.

Beyond volume, the scale of the increase matters for three reasons:

- Market balance: Türkiye's output contributes materially to easing global supply tightness after years of shortage.

- Trade leverage: Higher exportable surplus improves Türkiye's positioning in price-sensitive markets, particularly where EU supplies remain volatile.

- Strategic agriculture: The figures underline the growing role of Türkiye's olive sector as a buffer against climate-driven fluctuations elsewhere in the Mediterranean.

Table olives reinforce Türkiye's role

The IOC also highlights strong growth in table olive production, with global output estimated at over 3.3 million tonnes in 2024/25. Türkiye is again cited among the countries recording notable increases, reinforcing its dual importance across both olive oil and table olive markets.

Prices: easing, but uneven

Producer prices for extra virgin olive oil have begun to ease from recent peaks, though the IOC data show significant regional variation. Mid-December price levels ranged from around €430 per 100 kg in Spain to over €650 per 100 kg in Italy, reflecting differences in quality, stock levels, and domestic supply conditions.

For consumers, the production rebound points to gradual relief rather than a rapid price reset. For producers, it signals a return to competitive pressure after an exceptional period driven by scarcity.

What this means going forward

The IOC's latest figures suggest that the global olive oil market is moving out of an acute supply shock and into a phase where volume, efficiency, and trade strategy regain importance. For Türkiye, the data confirm a structural shift rather than a one-off spike: production scale now places the country among the key actors shaping global balance, not merely responding to it.

Future risks remain. Climate volatility, water stress, and input costs continue to weigh on the sector. But the current cycle demonstrates that Türkiye's olive industry has become a central variable in how global olive markets absorb shocks and adjust prices.